Enhancing the Iraqi Oil Revenue Forecasting: Comparative Evaluation of the ARIMA Model Extensions and Hybrid Models

DOI:

https://doi.org/10.62933/sck5bg17Abstract

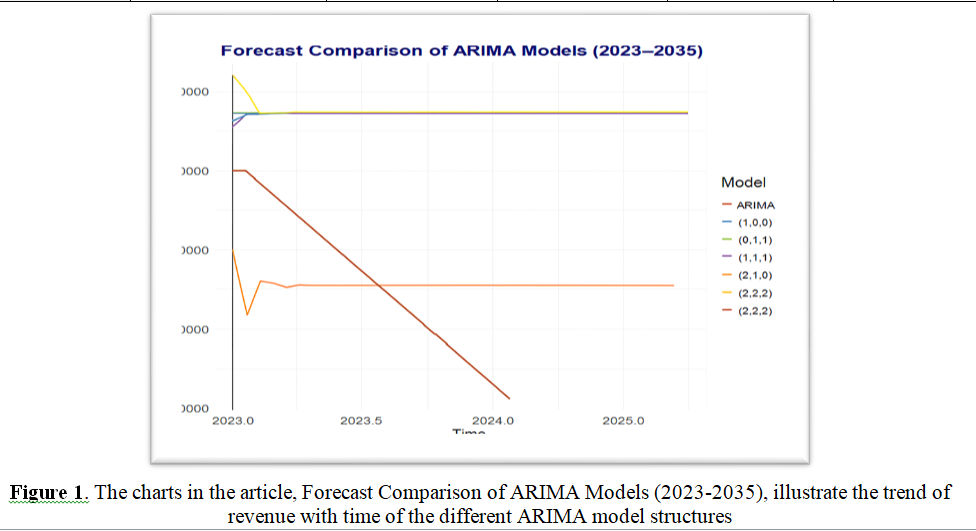

The current study provides the necessary response to the problem of oil revenue prediction errors in Iraq because it explicitly analyzes the extensions of the autoregressive integrated moving average model (ARIMA) and the hybrid methodology. Although the results of the existing studies have already proven the efficacy of simple ARIMA structures, there remains the gaps in the understanding on how the more sophisticated alterations and hybrid approaches could further enhance predictive accuracy. We engage in a full comparative study of extensions of ARIMA models such as seasonal adjustment, integration of exogenous variables, and hybrid models that integrate machine learning and the traditional time series models. The suggested approaches are operated on monthly data on Iraqi oil revenues between 2021 and 2023 and tested with harsh methods of validation in form of calculation including AIC, BIC, MAE and MAPE. The findings indicate that the hybrid models are more successful than the single ARIMA models by reducing the MAPE by 15%. Moreover, residual diagnostics verify the stability of these hybrid methods where there is no severe autocorrelation and the properties of error distribution are improved. The research adds to the literature in that it provides empirical data on effectiveness of hybrid forecasting method in volatile commodity markets giving decision makers more valid instruments to use in financial planning. In addition, the results also underscore the need to have a combination of statistical and machine learning paradigm to identify complex non-linear trends on oil revenue data. Besides the contribution to the methodological discussion of time series forecasting, the given research also offers some practical insights.

References

References

[1] AA Kubursi (1988) Oil and the Iraqi economy. Arab Studies Quarterly.

[2] MA Sualihu, M Amidu, T Assogbavi, et al. (2023) Financial planning and forecasting in the oil and gas industry. The Economics of the Oil Industry.

[3] HKR Al-Sammarraie, et al. (2024) Using a Hybrid Model (EVDHM-ARIMA) to Forecast the Average Wheat Yield in Iraq. Journal of Economics and Administrative Sciences for Iraq.

[4] EC Chukwuma-Eke, et al. (2022) A conceptual approach to cost forecasting and financial planning in complex oil and gas projects. Unable to determine the complete publication venue.

[5] S Sari-hassoun, N Boudjourfa, et al. (2025) Forecasting the Weekly Spot Oil Price Using a Hybrid Model ARMA-GARCH-MLP and Prophet Forecasting Method. Economic Computation & Cybernetics Studies & Research.

[6] BH Shehab & ZY Hussein (2022) MANAGING OIL REVENUES WITHIN THE FRAMEWORK OF THE IRAQI FINANCIAL MANAGEMENT LAW NO.(6) OF THE AMENDED 2019. ijrssh.com.

[7] FR Alharbi (2023) Gulf Cooperation Council Countries' Electricity Sector Forecasting: Consumption Growth Issue and Renewable Energy Penetration Progress Challenges. search.proquest.com.

[8] H Al-Ali (2012) Towards establishing a viable macroeconomic and medium-term fiscal framework integrated approach for the Iraqi economy. International Journal of Contemporary Iraqi Studies.

[9] GEP Box, GM Jenkins, GC Reinsel & GM Ljung (2015) Time series analysis: forecasting and control. books.google.com.

[10] H Alrweili & H Fawzy (2022) Forecasting crude oil prices using an ARIMA-ANN hybrid model. J Stat Appl Probab.

[11] P Sadorsky (2006) Modeling and forecasting petroleum futures volatility. Energy economics.

[12] A Camara, W Feixing & L Xiuqin (2016) Energy consumption forecasting using seasonal ARIMA with artificial neural networks models. Unable to determine the complete publication venue.

[13] RK Paul (2015) ARIMAX-GARCH-WAVELET model for forecasting volatile data. Model Assisted Statistics and Applications.

[14] PF Pai & CS Lin (2005) A hybrid ARIMA and support vector machines model in stock price forecasting. Omega.

[15] AA Pierre, SA Akim, AK Semenyo & B Babiga (2023) Peak electrical energy consumption prediction by ARIMA, LSTM, GRU, ARIMA-LSTM and ARIMA-GRU approaches. Energies.

[16] A Safari & M Davallou (2018) Oil price forecasting using a hybrid model. Energy.

[17] H Awijen, H Ben Ameur, Z Ftiti & W Louhichi (2025) Forecasting oil price in times of crisis: A new evidence from machine learning versus deep learning models. Annals of Operations Research.

[18] L Anning, AS Tuama & S Darko (2017) Inflation, unemployment and economic growth: evidence from the var model approach for the economy of Iraq. Unable to determine the complete publication venue.

[19] RA Abdlaziz, YA Ahmed, BA Mohammed, et al. (2022) The Impact of Oil Price Shocks on Economic Growth-Iraq A Case Study for The Period (1968-2019) Using Symmetric and Asymmetric Co-Integration Analysis. Qalaai Zanist Journal.

[20] HK Arora & DJ Smyth (1990) Forecasting the developing world: An accuracy analysis of the IMF's forecasts. International Journal of Forecasting.

[21] LC Kumins (2004) Iraq Oil: Reserves, Production, and Potential Revenues. policyarchive.org.

[22] B Lin, OE Omoju & JU Okonkwo (2015) Will disruptions in OPEC oil supply have permanent impact on the global oil market?. Renewable and Sustainable Energy Reviews.

[23] MG Salameh (2013) Iraq: An Oil Giant Constrained by Infrastructure & Geopolitics. papers.ssrn.com.

[24] E Antwi, EN Gyamfi, KA Kyei, R Gill & AM Adam (2022) Modeling and forecasting commodity futures prices: decomposition approach. IEEE Access.

[25] M Bilal, M Aamir, S Abdullah & F Khan (2024) Impacts of crude oil market on global economy: Evidence from the Ukraine-Russia conflict via fuzzy models. Heliyon.

[26] M Audi (2024) Exploring fiscal dynamics between resource and non-resource tax revenues in oil-dependent countries. Journal of Energy and Environmental Policy Options.

[27] T Naccache (2011) Oil price cycles and wavelets. Energy Economics.

[28] AH Cordesman (1999) Geopolitics and energy in the Middle East. Center for Strategic and International Studies.

[29] GP Herrera, M Constantino, BM Tabak, H Pistori, JJ Su, et al. (2019) Long-term forecast of energy commodities price using machine learning. Energy.

[30] C Glanois, P Weng, M Zimmer, D Li, T Yang, J Hao, et al. (2024) A survey on interpretable reinforcement learning. Machine Learning.

[31] SC Hillmer & A Trabelsi (1987) Benchmarking of economic time series. Journal of the American Statistical Association.

[32] R Dibie, FM Edoho & J Dibie (2015) Analysis of capacity building and economic growth in sub-Saharan Africa. Journal of Business and Social Science.

[33] Z Cui, W Chen & Y Chen (2016) Multi-scale convolutional neural networks for time series classification. arXiv preprint arXiv:1603.06995.

[34] A Ghorbel, M Abbes Boujelbene, et al. (2014) Behavioral explanation of contagion between oil and stock markets. International Journal of Emerging Markets.

Health economic evaluations using decision analytic modeling: principles and practices—utilization of a checklist to their development and appraisal

[35] J Soto (2002) Health economic evaluations using decision analytic modeling: principles and practices—utilization of a checklist to their development and appraisal. International Journal of Technology Assessment in Health Care.

Downloads

Published

Issue

Section

License

Copyright (c) 2026 Mustafa Habib Mahdi (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.

Licensed under a CC-BY license: https://creativecommons.org/licenses/by-nc-sa/4.0/