Estimate a nonparametric copula density function based on probit and wavelet transforms

DOI:

https://doi.org/10.62933/mt7r7d88Keywords:

Wavelets, Copulas, Wavelet Transforms, Probit transforms, Boundary effectsAbstract

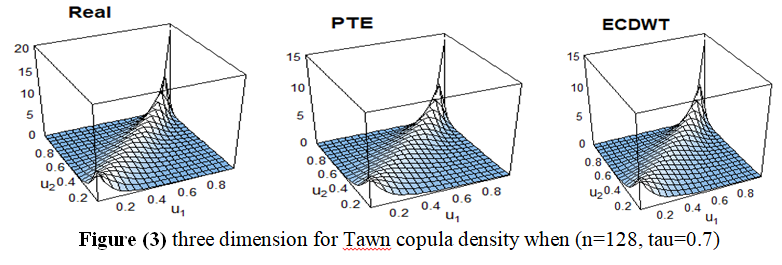

This study employs wavelet transforms to address the issue of boundary effects. Additionally, it utilizes probit transform techniques, which are based on probit functions, to estimate the copula density function. This estimation is dependent on the empirical distribution function of the variables. The density is estimated within a transformed domain. Recent research indicates that the early implementations of this strategy may have been more efficient. Nevertheless, in this work, we implemented two novel methodologies utilizing probit transform and wavelet transform. We then proceeded to evaluate and contrast these methodologies using three specific criteria: root mean square error (RMSE), Akaike information criterion (AIC), and log-likelihood (LogL). The wavelet transform method works better than the probit transform method at all three levels of correlation, as shown by a simulated study with four types of copulas, five sample sizes, and three levels of correlation. Research has demonstrated that probit transformation methods are most appropriate for linkages involving large and medium sample sizes, as indicated by Frank, Joe, and Tawn Copula. On the other hand, for copula functions for all sample sizes, the wavelet transform method was found to be ideal in cases with low correlation values

References

Deheuvels, P. (1979). La fonction de dépendance empirique etses propriétés. Un test non paramétrique d'indépendance. Bulletins de l'Académie Royale de Belgique,vol. 65,no.1, PP 274-292.

Hmood, M.Y (2005).Comparing Nonparametric Estimators For Probability Density Estimation. PhD thesis, University of Baghdad, Baghdad.

Dawod,E.A.A.(2006) .Using the Copula theory for Analyzing the Bivariate survival Function. PhD thesis, University of Baghdad, Baghdad.

Genest, C., and Favre, A. C. (2007). Everything you always wanted to know about copula modeling but were afraid to ask. Journal of hydrologic engineering, vol.12,no.4, pp347-368.

Omelka, M., Gijbels, I., and Veraverbeke, N. (2009). Improved kernel estimation of copulas: weak convergence and goodness-of-fit testing. The Annals of Statistics, vol.37,no.5B,pp 3023-3058.

Chaloob,I.H.(2011).Finding Bivariate distribution by using different copulas Function with Application in Biotical Field. PhD thesis, University of Baghdad, Baghdad.

Geenens, G. (2014). Probit transformation for kernel density estimation on the unit interval. Journal of the American Statistical Association,vol.109,no.505, pp346-358.

Geenens, G., Charpentier, A., and Paindaveine, D. (2017). Probit transformation for nonparametric kernel estimation of the copula density. Bernoulli, vol.23,no.3, pp1848-1873.

Hmood, M. Y., and Hamza, Z. F. (2019). On the Estimation of Nonparametric Copula Density Functions. International Journal of Simulation-Systems, Science & Technology, vol.20,no.2,pp1-7

Nagler,T.(2021)"Packge Kde vine , Multivariate kernel density Estimation with vine copula " URL https://github.com/tnagler/Kde vine.

Dawod,L.A-J.(2022).Structural Reliability Analysis Techniques with Multidimensional Correlation with Application. PhD thesis, University of Baghdad, Baghdad.

Jawad LB, Abdullah LT. Wavelet analysis of sunspot series. J Econ Finance Adm Sci. 2007;13(45):273-87.

AlDoori EA, Mhomod E., Hazard Rate Estimation Using Varying Kernel Function for Censored Data Type I, Baghdad Sci.J. 2019 Sep. 23;16(3(Suppl.)):0793 https://doi.org/10.21123/bsj.2019.16.3(Suppl.).%25p

Hassan YA, Hmood MY. Estimation of return stock rate by using wavelet and kernel smoothers. Period. Eng. Nat. Sci. 2020 Apr 27;8(2):602-12. http://dx.doi.org/10.21533/pen.v8i2.1195

Hmood MY, Hamza AH. Discrete wavelet based estimator for the Hurst parameter of multivariate fractional Brownian motion. In J. Phys.: Conf. Ser. 2021 May 1; 1879(3): 032033. https://doi.org/10.1088/1742-6596/1879/3/032033

Ansari J, Rüschendorf L. Sklar’s theorem, copula products, and ordering results in factor models. Depend Model. 2021 Oct 18;9(1):267-306. DOI: https://doi.org/10.1515/demo-2021-0113.

Cherubini, U., Luciano, E., and Vecchiato, W. (2004). Copula methods in finance. John Wiley & Sons.

Nelsen, R. B. (2006). An introduction to copulas. Springer Science & Business Media.

Alsina, C., Schweizer, B., and Frank, M. J. (2006). Associative functions: triangular norms and copulas. Copyright © by World Scientific Publishing Co.Pte.I.td

Zeng,X., Ren, J., Sun, M.,Marshall,S., and Durrani,T. (2014). Copulas for statistical signal processing (Part II): Simulation, optimal selection and practical applications. Signal processing, 94, 681-690.

Chen, L., and Guo, S. (2019). Copulas and its application in hydrology and water resources. Springer Singapore

André, L. M. B. C. M. (2019). Copula models for dependence: comparing classical and Bayesian approaches (Doctoral dissertation).Unversdade Delisboa.

[23] Hmood,M. Y., Abbas, T. M. and Nayef,Q. N.(2008). Nonparametric estimation of A Multivariate Probability Density Function , Al-Nahrain University Journal ,vol.11,no.2, pp55-63.

Gramacki, A. (2018). Nonparametric kernel density estimation and its computational aspects (Vol. 37). Cham: Springer International Publishing.

Charpentier, A., Fermanian, J. D., and Scaillet, O. (2006). The estimation of copulas: Theory and practice. Copulas: From theory to application in finance, Ensae-Crest and Katholieke Universiteit Leuven; BNP-Paribas and Crest; HEC Genève and Swiss Finance Institute.

Scott D.W. (2009). Multivariate Density Estimation: Theory, Practice, and Visualization, Papers, No.2004,16. New York: John Wiley & Sons.

Gijbels, I., and Mielniczuk, J. (1990). Estimating the density of a copula function. Communications in Statistics-Theory and Methods, vol.19,no.2, pp445-464.

Bean, A. T. (2017). Transformations and Bayesian Estimation of Skewed and Heavy-Tailed Densities (Doctoral dissertation, The Ohio State University).

Ranta M.Wavelet multiresolution analysis of financial time series. Finland: Vaasan yliopisto(2010) Apr.

Hmood MY, Hassan YA. Estimate the Partial Linear Model Using Wavelet and Kernel Smoothers. J. Econ. Finance Adm. Sci. 2020;26(119):428–443. https://doi.org/10.33095/jeas.v26i119.1892

Labat D. Recent advances in wavelet analyses: Part 1. A review of concepts. J. Hydrol. 2005 Nov 25;314(1-4):275-88. https://doi.org/10.1016/j.jhydrol.2005.04.003

Labat D, Ronchail J, Guyot JL. Recent advances in wavelet analyses: Part 2—Amazon, Parana, Orinoco and Congo discharges time scale variability. J. Hydrol. 2005 Nov 25;314(1-4):289-311. https://doi.org/10.1016/j.jhydrol.2005.04.004

Chui CK. An introduction to wavelets. 1st ed. United States: Academic press; 1992 Jan 1.

Chatrabgoun O, Parham G. Copula density estimation using multiwavelets based on the multiresolution analysis. Communications in Statistics-Simulation and Computation. 2016 Oct 20;45(9):3350-72. https://doi.org/10.1080/03610918.2014.944655

Mohammed AT. Nonparametric Estimation of Hazard Function by Using Wavelet Transformation [PhD Thesis]. Baghdad: University of Baghdad; 2019.

Hmood MY, Hibatallah A. Continuous wavelet estimation for multivariate fractional Brownian motion. Pak J Stat Oper Res. 2022 Sep 10; 18(3):633-41. https://doi.org/10.18187/pjsor.v18i3.3657

Rashid DH, Hamza S, K Comparison some of methods wavelet estimation for non-parametric regression function with missing response variable at random. J Econ Finance Adm Sci 2016; 22:382-406.

Kaiser G. A Friendly Guide to Wavelets. Springer Science & Business Media; 2010 Nov 3. https://doi.org/10.1007/978-0-8176-8111-1

Genest C, Masiello E, Tribouley K. Estimating copula densities through wavelets. Insurance: Mathematics and Economics. 2009 Apr 1;44(2):170-81. https://doi.org/10.1016/j.insmatheco.2008.07.006

Daubechies I. Ten lectures on wavelets. Philadelphia, PA: SIAM; 1992 Jan 1. https://doi.org/10.1137/1.9781611970104

Meyer Y. Wavelets and Operators: Volume 1. United Kingdom: Cambridge university press; 1992. https://doi.org/10.1017/CBO9780511623820

Downloads

Published

Issue

Section

License

Copyright (c) 2024 Fatimah Hashim Falhi, Munaf Yousif Hmood (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.

Licensed under a Creative Commons Attribution 4.0 International License: https://creativecommons.org/licenses/by/4.0/